Summary: Debtor financing is an umbrella term products that finance your accounts receivable. The two most common products are invoice financing and invoice discounting. This article helps you understand the rates and fees associated with these two solutions. This article assumes that you are familiar with how factoring and invoice discounting work. We cover the following information:

- Invoice finance vs. invoice discounting

- Transaction costs

- How are rates determined?

- Sample transaction

1. Invoice financing vs. Invoice Discounting

Invoice financing and invoice discounting both provide financing to companies that have cash flow problems. They help companies that offer net 30-day payment terms to their clients but need to get paid sooner. However, both solutions operate differently.

Most invoice finance programmes provide credit and collections services alongside the financing platform. Invoice discounting, on the other hand, offers only financing.

Invoice financing, also known as factoring, is typically offered to smaller companies that don’t have established finance departments. Invoice discounting, on the other hand, is offered to larger companies that have established financial controls. To learn more about both solutions, read “What is Debtor Financing? How does it work?”

2. Transaction costs

Most invoice financing and invoice discounting proposals have all or some of the fees discussed in this section. Keep in mind that proposals may use different terminology and that actual costs are highly individualised.

a. Due diligence fee

The due diligence fee covers the costs of performing credit reviews, filings, and work necessary to establish a financing line for your company. This fee is paid if you accept the financing proposal.

The cost of this fee can range from a few hundred to a few thousand dollars, depending on the complexity of the situation and the size of the line. Generally, larger companies or more complex situations have higher due diligence costs.

b. Administration Fee

The administration fee, also known as a service fee, is an ongoing charge. It is charged on the total value of every invoice that is financed. This fee can range from 0.80% – 2.50%. Usually, higher lines have lower rates. We explain this in more detail in the next section. The following table provides approximate administration fees for different line sizes.

| Line Size | Administration Fee (Rate) |

|---|---|

| $50,000 | 2.00% – 2.50% |

| $200,000 | 1.35% – 1.75% |

| $500,000 | 0.80% – 1.25% |

Note: This table can be scrolled left/right on mobile devices

c. Interest rate

The interest rate, also known as the discount fee, is an ongoing charge applied to the advanced funds. The interest rate varies by company and is typically based on a reference rate, which is then adjusted according to market conditions and transaction risk.

This rate can range from 11.35% to 14.85% per annum, depending on the transaction details. The interest rate is charged daily from the time the invoice is financed until your customer pays it.

Proposals typically provide the yearly rate through the charge is applied daily. Consequently, you will need to divide the interest rate by 365 to determine the daily rate. The following table provides approximate interest rates for different line sizes.

| Line Size | Advance Rate | Base Rate | Add/Subtract | Financing Rate |

|---|---|---|---|---|

| $50,000 | 70% – 85% | 12.85% | 1.5% to 2% | 14.35% to 14.85% |

| $200,000 | 70% – 85% | 12.85% | -0.5% to 1.5% | 12.35% to 14.35% |

| $500,000 | 70% – 85% | 12.85% | -1.5% to 0% | 11.35% to 12.85% |

Note: This table can be scrolled left/right on mobile devices

d. Minimum fee

Debtor finance companies typically provide better prices to clients who agree to finance a high volume of invoices. In these cases, a proposal may have a minimum fee.

The minimum fee applies only if you don’t finance the volume of invoices that you agreed to. Generally, it covers the difference between what your company financed vs. what it agreed to finance.

e. Debtor protection

This is an optional service that covers you if your customer does not pay an invoice. This service is similar to trade credit insurance. The average cost is typically 0.50% of the invoice amount. Note that debtor protection does not cover you if an invoice is subject to a dispute.

3. How are rates determined?

Debtor finance company determine your rates based on the size of the line, the transaction’s risk profile, and market conditions. Let’s examine these in more detail.

a) Size of the line

Debtor finance is a volume business. Consequently, the line’s size has the most significant influence on your rates. Larger companies with high turnovers will have the most negotiating leverage.

b) Credit quality of invoices

The credit quality of your invoices is important and used to determine whether the company is willing to finance the invoice. While it can influence your rates, it is not as significant as volume.

c) Other considerations

Debtor financing companies also take company health, market conditions, and your industry into consideration. For example, companies in industries with lower-risk transactions (e.g., labour hire) will often receive better terms than companies in industries with more challenging transactions (e.g., trade contractors).

4. Sample transaction

The best way to understand how these costs are calculated is to work through an example. For simplicity, the example assumes the transaction only has a single invoice that is paid in exactly 30 days. We will only cover the administration fee and the interest rate fee since these are the most important costs.

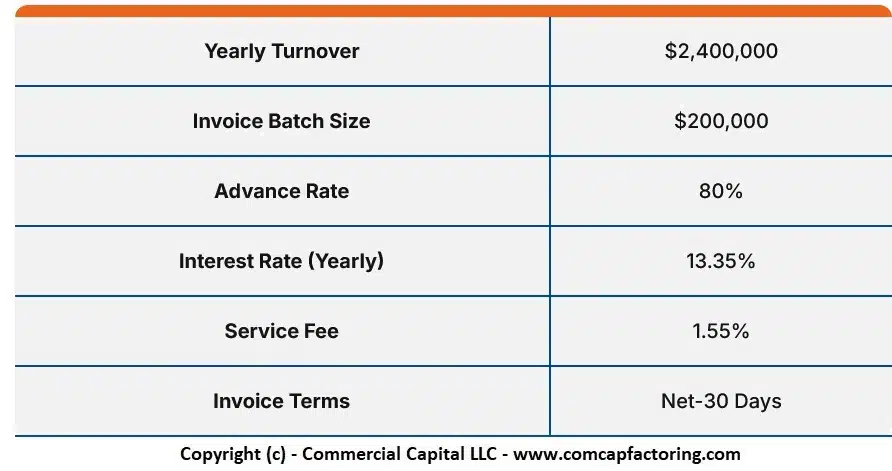

The following table shows the transaction details for this example.

| Yearly Turnover | $2,400,000 |

| Invoice Batch Size | $200,000 |

| Advance Rate | 80% |

| Interest Rate (Yearly) | 13.35% |

| Service Fee | 1.55% |

| Invoice Terms | Net-30 Days |

Note: This table can be scrolled left/right on mobile devices. Click here for an image of the table.

{kind=link}

a) The advance

The debtor finance company receives the $200,000 invoice the client wants to finance. The finance company processes the invoice and deposits the $160,000 advance into your company’s bank account

The advance is calculated by multiplying $200,000 by 80%, which equals $160,000. The remaining $40,000, less the financing fees, will be deposited once the invoice is paid in full.

b) Settlement and second instalment

The end customer pays the invoice within 30 days. This payment initiates the settlement process for the transaction.

The debtor finance company calculates the settlement amount by subtracting the $4,485.60 financing cost from the remaining $40,000 that was not advanced. The remaining $35,514.40 is deposited into your bank account to close the transaction.

The total financing cost of $4,855.60 is determined by adding the administration fee to the interest rate fee. The following table explains how these costs are calculated.

| Fee | Total | Calculation |

|---|---|---|

| Administration Fee | $3,100.00 | $200,000 x 1.55% |

| Interest Rate Fee | $1,755.60 | (13.35%/365 days) x 30 days x $160,000 |

Note: This table can be scrolled left/right on mobile devices

i) Administration fee calculation

The administration fee calculation is straightforward. Multiply the $200,000 invoice amount by 1.55%,which totals $3,100.

ii) interest rate fee calculation

The interest rate fee calculation is based on the $160,000 advanced (i.e., utilised funds). Calculating this cost takes three steps. The first step is to calculate the daily rate. To calculate this rate, divide the 13.35% interest rate by 365 (number of days in a year). This calculation yields a daily rate of 0.037%.

The next step is to multiply the daily rate of 0.037% by the $160,000 advance to determine the daily cost. This calculation yields a daily cost of $58.52.

Lastly, multiply the $58.52 daily cost by 30 days, which is the number of days the invoices were open. This calculation totals $ 1,755.60 (Note: We rounded some figures for clarity. Your calculation may differ by a few cents).

iii) Total financing cost calculation

Calculate the total financing cost by adding the $3,100 administration fee to the $1755.60 interest rate fee. This calculation yields a total financing cost of $4,855.60.

Need a debtor financing quote?

We are a leading provider of debtor finance and can provide you with a competitive quote. For an instant quote review, fill out the enquiry form.

Marco Terry is the Managing Director of Commercial Capital LLC and has over two decades of experience in asset-based finance. He has worked with small and mid-sized companies across the United States, Canada, and Australia. Marco holds a Master of Science in Finance.