This article explains how to invoice financing fees work and how much it costs to use the programme. It also provides an example that shows how these fees are calculated and how they are applied. You will learn the following:

- How invoice finance works

- Typical rates and advances

- How fees are calculated

- How establishment fees work

1. How does invoice finance work?

This article assumes that you are already familiar with invoice finance and know how it works. Here is a short summary of the programme.

Invoice financing companies provide cash flow by purchasing your invoices, typically in two instalments. The first instalment is called the advance and covers 70% to 85% (varies) of the invoice. It is deposited into your bank account soon after you submit the invoice to the finance company.

The remaining 15% to 30%, less applicable fees, is deposited to your account once the invoice is paid in full. This instalment settles the transaction.

2. Typical rates and fees

Most invoice financing lines have an administration fee and an interest rate fee that are based on the line’s utilisation. Additionally, some facilities may include an optional debtor protection service fee. This service, similar to trade credit insurance, protects approved invoices from default.

a) Administration Fee

The administration fee covers the cost of the finance company’s services for managing and operating the line. It is determined by the credit limit and applied to every invoice that is submitted in a month. The following table shows approximate administration fees for lines of three different size.

| Line Size | Administration Fee (Rate) |

|---|---|

| $50,000 | 2.00% – 2.50% |

| $200,000 | 1.35% – 1.75% |

| $500,000 | 0.80% – 1.25% |

b) Interest rate fee

The interest rate fee is applied to the advanced portion (i.e., the “utilised funds”) of every open invoice. It is determined daily on a pro-rata basis. The interest rate fee starts when an invoice is processed. It ends once the end customer pays the invoice.

Finance companies typically determine this rate using a base rate that is adjusted according to your line’s credit limit and quality. Invoice financing is a volume based business. Larger lines typically have lower costs.

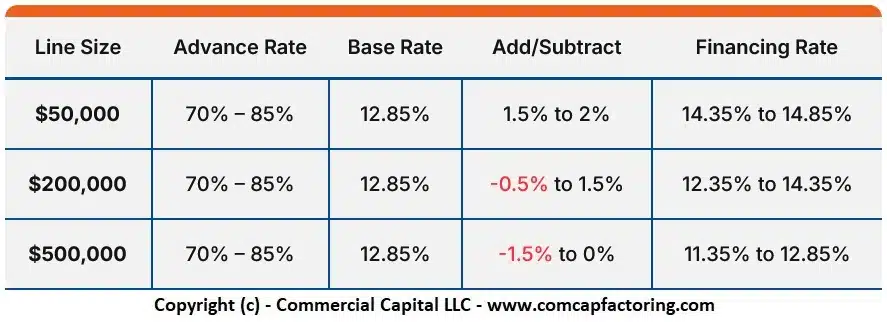

The base rate varies by finance company, but it’s usually a combination of a reference rate (e.g., BBSY), the firm’s cost of capital, and market conditions. The following table shows the rate details for three example line sizes.

| Line Size | Advance Rate | Base Rate | Add/Subtract | Financing Rate |

|---|---|---|---|---|

| $50,000 | 70% – 85% | 12.85% | 1.5% to 2% | 14.35% to 14.85% |

| $200,000 | 70% – 85% | 12.85% | -0.5% to 1.5% | 12.35% to 14.35% |

| $500,000 | 70% – 85% | 12.85% | -1.5% to 0% | 11.35% to 12.85% |

Note: Table can be scrolled left/right on mobile devices. Tap on screen if scrollbar does not appear. Click here for an image of the table.

{kind=link}

c) Debtor Protection

Some finance companies offer debtor protection, which is similar to trade credit insurance This optional service covers unpaid invoices if your customer is unable to pay.

Note that this service does not cover invoices subject to disputes. It can go from 0.30% to 0.50%, depending on the credit quality of your invoice and market conditions.

d) Minimum Fee

Invoice finance lines often have a minimum administration fee. The fee covers the cost of operating the line and is applied only if the line is underutilised. Minimums are negotiable and can be adjusted based on market or business conditions (e.g., seasonal businesses).

The minimum fee only applies if your monthly administration fees are below a set amount. If this happens, your business needs to pay the difference between the actual administration fees for that month and the minimum fee.

3. How to calculate the cost of invoice finance

The best way to understand how these fees are calculated is through an example. Let’s assume a business is financing its invoices using the following terms.

| Credit Limit | $200,000 |

| Advance / Leverage | 80% |

| Administration Fee | 1.50% |

| Interest Rate | 13% |

| Debtor Protection | 0.40% |

The business decides to finance a $50,000 invoice on the first day of the month. The invoice is paid by the end customer after 35 days. The following sections show how the fees are calculated and applied.

a) Administration fee

The $50,000 invoice is subject to an administration fee of 1.50%, which equals $750. The following table shows how this is calculated.

| Invoice Amount | Administration fee (Rate) | Cost |

|---|---|---|

| $50,000 | 1.50% | $750 |

b) Interest rate

The proposed advance (leverage) on the $50,000 invoice is 80%. This works out to $40,000. This advance is deposited into your bank account as soon as the financier processes the invoice.

The interest rate is charged daily so you need to convert the 13% yearly interest into a daily charge. To calculate the daily fee, divide 13% by 365 days, which equals 0.0356%

| Interest Rate | Days in Year | Daily Rate |

|---|---|---|

| 13% | 365 | 0.0356% |

In the example, the invoice is paid in 35 days. The total interest fee is calculated by applying the 0.0356% daily fee to the $40,000 advance and multiplying by 35 days. This calculation totals $498.63

| Advanced Amount | Days | Daily Fee (Rate) | Total Fee |

|---|---|---|---|

| $40,000 | 35 | 0.0356% | $496.63 |

c) Debtor protection

To calculate the debtor protection fee, multiply 0.40% by $50,000, which is the invoice’s face value. This fee amounts to $200.

d) Total cost calculation

To determine the total cost of financing the invoice, add the $750 administration fee, the $498.63 interest rate cost, and the $200 debtor protection fee (if used). This works out to $1,448.63.

The debtor protection fee is optional, so the following table shows the costs with and without this protection.

| Administration Fee | $750 |

| Interest Fee | $498.63 |

| Debtor Protection | $200 |

| Total (All Services) | $1,448.63 |

| Total (w/o Debtor Protection) | $1,248.63 |

4. Establishment fees

Financiers charge a fee to cover the expense of establishing the invoice finance line and for the initial disbursement. Both are one-time fees.

a) Establishment fee

The establishment fee covers the costs of underwriting and setting up the facility. It is determined by the size of your credit line and the complexity of the transaction.

The establishment fee is charged only if you accept the finance company’s proposal and decide to move forward.

| Line Size | Establishment Fee |

|---|---|

| $50,000 | $500 – $1250 |

| $200,000 | $1,500 – $2,000 |

| $500,000 | $2,000 – $5,000 |

b) Settlement fee

The settlement fee is similar to the administration fee. It is charged only when setting up the line and disbursing the funds. The fee covers the initial setup of the ledger, debtor setup, etc.

Need an invoice finance quote?

We are a leading provider of invoice finance in Australia. For a quote, fill out the enquiry form. A representative will contact you shortly.

Note: This information is presented for educational/informational purposes only. The rates and costs are examples and apply to hypothetical transactions.

Marco Terry is the Managing Director of Commercial Capital LLC and has over two decades of experience in asset-based finance. He has worked with small and mid-sized companies across the United States, Canada, and Australia. Marco holds a Master of Science in Finance.