Summary: This article provides an overview of the typical financing rates for the two leading debtor finance products. It explains how debtor financing companies determine your rates and how those rates are applied in a transaction. We cover the following information:

- Invoice finance vs. invoice discounting

- What determines the cost of a transaction?

- Rate components

- Sample transaction

If you are not familiar with debtor financing, read “What is Debtor Financing?” to learn more.

1. Invoice financing vs. invoice discounting

Debtor financing is an umbrella term used for products that finance a company’s accounts receivable. The most widely used debtor finance products are invoice financing and invoice discounting.

Invoice financing is suited for small and growing companies that have cash flow problems due to slow-paying invoices. Invoice discounting, on the other hand, is best suited for companies that have:

- Achieved consistent profitability

- Reliable financial controls

- A yearly turnover in excess of $3,000,000

The difference between both products is operational and in their qualification requirements. The cost of an invoice financing line is similar to the cost of a comparably sized invoice discounting line. Read “How does debtor finance work?” to learn more.

2. What determines the cost of a transaction?

The interest rates for a transaction depend on two factors: your turnover volume and the risk associated with your invoices. Like most financial transactions, debtor financing is a volume-based business. Companies with high turnovers and low-risk invoices can negotiate lower rates.

When evaluating the risk of your transaction, debtor financing companies consider the following criteria:

- The credit quality of your invoices

- The number of customers you have (also known as concentration)

- The financial health of your company

- Industry-specific issues

3. Rate components

There is no standard pricing structure for the industry. However, most debtor finance companies charge two fees: the administration fee and the interest rate.

The administration fee, also referred to as a service fee, is a one-time charge applied to each submitted invoice. It’s based on the total value of the invoice. The following table provides approximate administration fees for different line sizes.

| Line Size | Administration Fee (Rate) |

|---|---|

| $50,000 | 2.00% – 2.50% |

| $200,000 | 1.35% – 1.75% |

| $500,000 | 0.80% – 1.25% |

The interest rate, also known as a discount fee, is charged on the advanced funds (e.g., utilised funds). It accrues daily and is charged monthly. The interest rate is typically based on a reference rate that is adjusted to reflect transaction size, risk, and market conditions.

The following table shows approximate costs for different-sized lines.

| Line Size | Advance Rate | Base Rate | Add/Subtract | Financing Rate |

|---|---|---|---|---|

| $50,000 | 70% – 85% | 12.85% | 1.5% to 2% | 14.35% to 14.85% |

| $200,000 | 70% – 85% | 12.85% | -0.5% to 1.5% | 12.35% to 14.35% |

| $500,000 | 70% – 85% | 12.85% | -1.5% to 0% | 11.35% to 12.85% |

Note: This table can be scrolled left/right on mobile devices.

4. Sample transaction

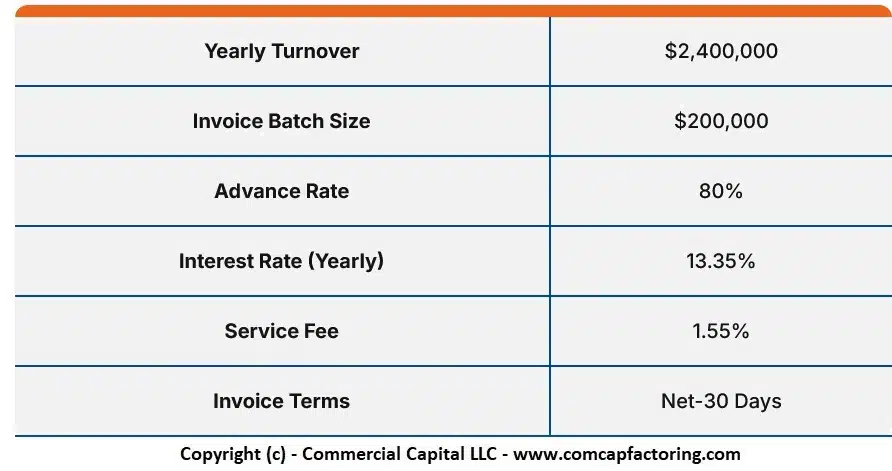

The easiest way to explain how debtor finance interest rates work is to review a sample transaction. Let’s assume that we have a client with the following characteristics:

| Yearly Turnover | $2,400,000 |

| Invoice Batch Size | $200,000 |

| Advance Rate | 80% |

| Interest Rate (Yearly) | 13.35% |

| Service Fee | 1.55% |

| Invoice Terms | Net-30 Days |

Note: Click here for an image of the table.

{kind=link}

After delivering services to its customers, the client submits a $200,000 batch of invoices to the debtor financing company. The finance company processes the batch and deposits the advance of $160,000 (80% x $200,000) to the client’s bank account.

After 30 days, the customers pay their invoices in full, which settles the specific batch. The debtor finance company rebates $35,144.38, which is the remaining $40,000 (20% x $200,000) that was not initially advanced, less the total fees of $4,855.62.

The cost is calculated as follows:

| Fee | Total | Calculation |

|---|---|---|

| Administration Fee | $3,100.00 | $200,000 x 1.55% |

| Interest Rate Fee | $1,755.62 | (13.35%/365 days) x 30 days x $160,000 |

Note: This table can be scrolled left/right on mobile devices.

To get the total fee, add the $3,100 service fee to the $1,755.62 interest cost. This sum equals $4,855.62.

Please note that this example oversimplifies the transaction for the sake of clarity. Invoices typically don’t get paid exactly 30 days after the due date. Some invoices are paid more quickly, while others may take longer.

However, this article should help you understand how debtor financing rates work. Learning this structure will help you determine if factoring or invoice discounting is the right solution for you.

Can we help you?

We are a leading debtor financing company and can provide high advances at competitive rates. For more information, fill out our enquiry form and a representative will contact you soon.

Note: This article is intended for informational purposes only. The numbers used here are not representative of an actual client.

Marco Terry is the Managing Director of Commercial Capital LLC and has over two decades of experience in asset-based finance. He has worked with small and mid-sized companies across the United States, Canada, and Australia. Marco holds a Master of Science in Finance.