Summary: Factoring is a type of financing that helps improve the cash flow of companies that have slow-paying invoices. This form of financing gives the client access to immediate funds, which can then be used to pay for business expenses and to grow.

In this article, we show you how factoring works. We go over every aspect that you need to know to determine if factoring is right for you. We cover the following subjects:

1. What is factoring?

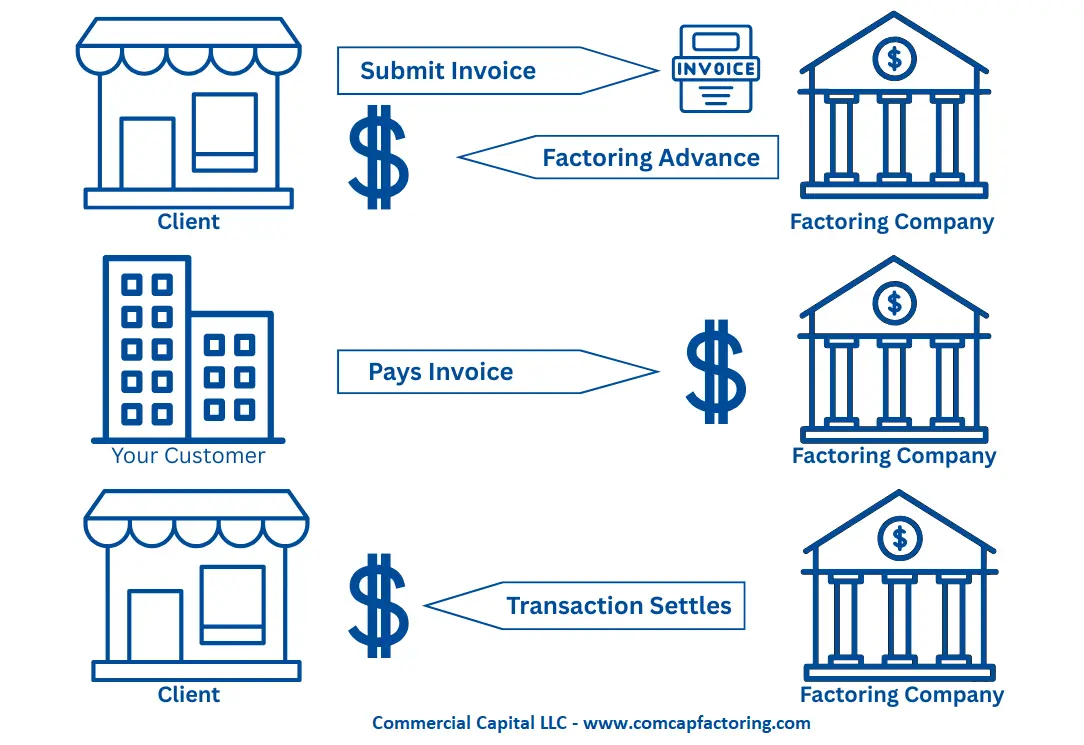

The process of factoring your receivables is relatively simple. It’s structured through the sale of your invoices to a factoring company. The factor buys your invoices and pays immediately for them. Consequently, you don’t have to wait 30 to 60 days to get paid by customers. This provides your company with immediate access to funds while the factor waits for your customers to pay.

Transactions settle once the factor receives a payment from your customer. Your customer pays their invoices on their usual terms of 30 to 60 days. Companies that use factoring often finance their invoices regularly. It provides an ongoing source of financing, improves liquidity, and provides a platform for growth.

Most factoring companies buy your invoices in two installments. The first installment is called the advance and covers about 80% of the invoice’s value. The advance is deposited in your bank account when you submit an invoice. Note that the advance percentage varies based on industry and risk profile and can range from 70% to 98%. The average advance is about 80%.

The remaining 20%, less the factoring fee, is paid once your customer pays the invoice in full. These funds are deposited to your bank account as a second installment. This payment settles the transaction.

2. How does it work?

In this section we cover everything your company needs to do to set up a factoring account and get funded. Setting up an account is a one-time process and usually takes a couple of days. After the account is set up, you are ready to finance invoices.

Invoices from existing customers can usually be funded the same day you submit them. However, these invoices must be submitted early enough during the day so the factor can process them. Otherwise, invoices are usually funded within a day or so.

Step 1: How to find a factoring company

Most factors are small to medium-sized companies that specialize in specific industries. It’s best to choose a factoring company that has experience in your industry.

Work with factoring companies that have been in business for a decade or more. This longevity shows that they have the financial wherewithal to survive economic cycles.

Step 2: Application and due diligence

The next step is to fill out and submit the financing application. Each factor has its own application process, though they are all similar. Factoring companies need the application to evaluate the transaction and determine if it’s a good fit for both parties. During their due diligence, factors evaluate if your:

- Customers have good credit

- Invoices are free from liens

- Company has no major problems

Due diligence is usually quick, and you can often get a proposal the same day you submit your application.

Step 3: Proposal and contract

The factoring company will send a proposal to you after they finish reviewing the transaction. Most proposals have three key pieces of information:

- Advance rate (1st installment)

- Factoring rate

- Length of term

Once you sign the proposal, the factor performs its final diligence and sends the contract to you. Once you sign the contract, your account is ready for first funding.

Step 4: Initial account setup

In this step, the factoring company sends a Notice of Assignment (NOA) to every customer whose invoices you want to factor. The NOA is a standard industry document and is used by every factor. It advises the customer’s accounts payable department how to handle invoice payments. This process is done once for each customer.

Step 5: Funding invoices

Every factor has its own submission process, though they are all similar. Usually, you submit the invoices you want to finance through an online portal or by email. Once the factor receives and verifies the invoices, they deposit the first installment (advance) in your bank account. You repeat this step every time you want to finance invoices.

Step 6: Settling transactions

Factors settle each transaction when your customers pay their invoices. Once paid, the factor remits the remaining 20% (less the fee) to you, as the second installment. This deposit settles the transaction.

3. Do I qualify for invoice factoring?

Qualifying for factoring is much easier than qualifying for other types of business financing. The main prerequisites are:

a) Your customers must have good commercial credit

This is the most important requirement to qualify for factoring. The transaction is built by leveraging the credit strength of your customers to your advantage.

b) Your invoices must be free of liens

Factoring companies provide financing by purchasing the financial rights to your invoices. Consequently, your invoices must be free of liens. Factors will buy only invoices for which they have a first-position PPSA or hypothèque.

c) Margins must be above 15%

It’s best to use this financing solution if your gross profit margins are at least 15%. If you are unsure, speak with your financial advisor.

d) You must have good invoicing practices

Having good invoicing practices is also an important requirement for financing your receivables. Your invoices must have well-defined payment terms and must have all the necessary backups to ensure smooth collections.

e) Tax issues must be manageable

A big advantage of receivables factoring over other solutions (e.g., business loans) is that it is available to companies with tax problems. However, these tax problems must be manageable and surmountable with financing. In these cases, a payment plan with the necessary tax authority may be required.

f) There must be no open bankruptcies

The company and the main owners must not have an active bankruptcy. Past bankruptcies must be properly discharged.

4. Is factoring right for me?

Although easy to get, invoice factoring is not for everyone. It is designed to solve a specific type of financial issue. You can determine if factoring will help you by asking yourself three questions. If any (or all) of these statements are true, factoring is probably the right solution for your company:

a) If customers paid quickly, your financial problems would go away

Most companies that finance their receivables do so because they have cash flow problems. These problems are always due to slow-paying customers. If getting paid sooner (through financing) would eliminate the majority of your financial problems, there is a good chance that factoring is right for you.

b) Customers keep asking for payment terms but you can’t offer them

Small and midsize companies often experience problems when their larger customers demand 30- to 60-day payment terms. Their financial reserves are not large enough to pay company expenses while also waiting for customer payments. This puts them in a bind. They can either turn away customers or offer terms while getting into a financial predicament.

c) You have turned away orders because you could not afford to fulfill them

There are times when a company must turn new orders away because it does not have the resources to service them. This scenario leaves customers with no other choice but to go to a competitor. Obviously, you want to avoid this situation at all costs. This problem is common for companies that have growing payrolls (e.g., staffing firms, consulting companies, etc.)

Get more information

We can provide you with high advances at low rates. For information, get an online quote or call (877) 300 3258.

Marco Terry is the Managing Director of Commercial Capital LLC and has over two decades of experience in asset-based finance. He has worked with small and mid-sized companies across the United States, Canada, and Australia. Marco holds a Master of Science in Finance.