Most factoring transactions are structured as the purchase of an invoice in two installments. The first installment, usually 70% to 90% of the invoice, is the factoring advance. The second installment, the remaining 15% to 30% (less fees), is the rebate and is usually paid once the customer pays the invoice in full. At least, that is the common explanation. The actual return of the reserve is a little bit more complex.

Factoring rebate vs. reserve

The rebate and the invoice factoring reserve are interlinked terms that are often confused, in part because the rebate is essentially the reserve, or a portion of it, being returned to the customer.

How does the rebate work?

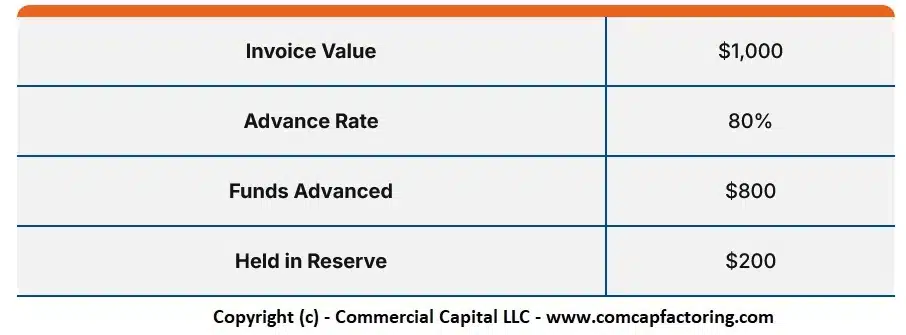

To better understand the rebate, you need to understand how the reserve works in accounts receivable factoring. Let’s look at a sample transaction with these parameters:

| Invoice Value | $1,000 |

| Advance Rate | 80% |

| Funds Advanced | $800 |

| Held in Reserve | $200 |

Note: Click here for an image of the table.

{kind=link}

Each factoring company has its own reserve policy. For example, some factors keep a permanent reserve equal to the value of a few invoices and then release any amount above that (the “excess reserve”). Others don’t hold a permanent reserve and release it immediately when an invoice is paid.

Understanding the factor’s reserve policy and reserve release schedule is important since both have critical implications on your cash flow. The following is a list of common reserve policies, but bear in mind they vary among factoring companies:

- Excess reserve is rebated when invoice is paid

- Excess reserves are released twice per month for paid invoices (e.g., on the 1st and the 15th)

- Excess reserves are released once per month

For more details on how transaction are structure, please read “How does invoice factoring work?“

Can we help you?

We are a leading factoring company and can offer competitive financing packages. For a quote, please fill out this form or call (877) 300 3258.

Marco Terry is the Managing Director of Commercial Capital LLC and has over two decades of experience in asset-based finance. He has worked with small and mid-sized companies across the United States, Canada, and Australia. Marco holds a Master of Science in Finance.