In this article, we discuss factoring rates and how to use rates to determine the total cost of using this solution. From this article, you will learn:

If you are not familiar with factoring, consider reading “How does factoring work?” before reading this article. If you just want an instant rate quote, try this form.

1. Average factoring rates and advances

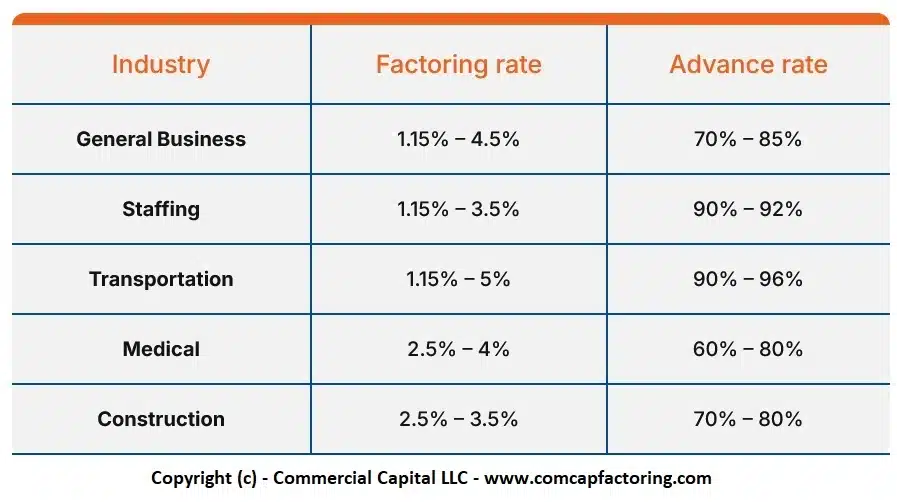

The following table gives you an idea of the range of rates and advances for some industries. The listed rates represent the average rate for 30 days. Rate costs are usually prorated based on how long your invoices take to pay, unless you have a flat fee schedule.

| Industry | Factoring rate | Advance rate |

| General Business | 1.15% – 4.5% | 70% – 85% |

| Staffing | 1.15% – 3.5% | 90% – 92% |

| Transportation | 1.15% – 5% | 90% – 96% |

| Medical | 2.5% – 4% | 60% – 80% |

| Construction | 2.5% – 4.5% | 70% – 80% |

Note: Click here for an image of the table.

{kind=link}

Factoring rates vary by industry, risk, transaction workload, and volume. Companies with lower risks whose receivables are easy to manage usually get lower rates and higher advances. Conversely, higher risk companies or companies whose receivables require substantial processing tend to have higher rates. We discuss this in detail in the next sections.

2. Flat rate vs. tiered rates?

Most factoring companies prefer to use a tiered rate structure. It allows them to link the cost of financing to the actual length of time the invoice is outstanding. With a tiered pricing model, the longer the invoice goes unpaid, the higher the cost. Tiered rates are quoted in a variety of formats. Examples include:

At the other end of the spectrum, some clients negotiate a flat rate. In this case, the client pays only the stated rate, regardless of how long the invoice takes to pay.

Both flat and tiered rates have pros and cons. You have to determine which one works best for your specific situation. Factors tend to use flat rates when your customers pay on predictable schedules. For example, you may get a flat rate if all your clients pay in 20 to 30 days, or if they all pay in less than 45 days.

3. What determines factoring rate?

The two most important criteria that determine your rate are the factor’s risk of buying your invoices and your financing volume. Low-risk clients that finance high sales volumes usually get the lowest rates. On the other hand, higher-risk clients or clients with a low sales volume usually get higher rates.

a) How is volume determined?

Factoring is a volume-based business, not unlike the wholesale business. Clients that need larger financing lines (i.e., higher volumes) get lower prices. Factoring volume is by far the most important variable used in determining your rate.

However, factoring companies also consider the size and number of invoices you have. Clients that need to process a high volume of low-value invoices may have higher-than-average costs. This is due to the amount of labor needed to process a high volume of low-value invoices.

b) Invoice size is important (an example)

For example, it’s easier for a factor to finance a single $30,000 invoice than it is to finance thirty $1,000 invoices, each to a different customer. Both scenarios total the same amount – $30,000. However, processing thirty invoices takes more work than processing one larger invoice.

While having small invoices affects your cost, it does so only to a certain extent. Let’s look at another example. Although financing ten $30,000 invoices is more work than financing a single $300,000 invoice, the rates would be similar. This is because the fees generated by each individual invoice are sufficient to cover their associated labor cost.

4. How is client risk determined?

Factoring companies evaluate risk differently. Some are more open to risk than others. However, they usually look at three factors to determine client risk:

a) Your industry

Factoring companies consider your industry when determining how to structure a proposal. Some industries are considered to have a lower risk. Consequently, they often get better terms. These industries include transportation, staffing, and consulting. On the other hand, some industries are seen as risky or require specialized knowledge from the factor. These often get higher rates and lower advances. These industries include construction and third-party medical paid healthcare.

b) The credit quality of your clients

The creditworthiness of your clients is very important. However, it does not play a large role in determining your financing rate. Instead, creditworthiness is used to decide whether or not an invoice from a customer will be funded. Your client’s creditworthiness also affects the size of your financing line and your advance percentage.

c) The stability of your business

Factoring companies consider the stability of your business in their rate decision. Companies with a reasonably long and stable history are considered safe. Consequently, they often get lower rates. New companies, or companies with unsteady sales, are considered riskier. Accordingly, they often get slightly higher rates.

5. Factoring cost vs. factoring rate

Businesses that are in the process of choosing a factoring company often focus their negotiation efforts on getting the best the rate. Although a competitive rate is important, it is only one component of your factoring cost.

A better alternative is to focus negotiations on the “total cost per dollar” of the proposal. This approach helps ensure you pay the lowest amount for each financed dollar. To calculate the total cost per dollar, you need two figures. You need the rate and the factoring advance.

In most cases, you get the best deal by negotiating the lowest possible rate at the highest possible advance. This assumes you are looking for the highest possible advance, which is the case for most business owners. Otherwise, adapt your strategy accordingly.

a) Cost of factoring vs. rate example

It’s easiest to explain this concept with an example. Let’s look at two possible scenarios. Which one has the lowest cost?

If you chose option #1, you are incorrect. This was a trick question. Though they have different rates and advances, they both have the same “cost per dollar.”

Dividing 3% by 70% (0.03/0.70) and multiplying by 100 (cents) gets you the cost per dollar of around $0.04 (4 cents). Likewise, 3.43% divided by 80% and multiplied by 100 cents yields the same result (0.0343/0.80 x 100).

If presented with these alternatives by two factoring companies, choose a proposal based on your cash flow needs. If a 70% advance is enough, go with option 1. If you need a higher advance, go with option 2. They have the same cost per dollar.

For more details of how to review cost, read “The True Cost of Factoring” or try our cost per dollar calculator.

6. Average factoring rates (Summary)

In summary, factoring rates range from 1.15% to 4.5% per 30 days. Advances range from 70% to 85%. There are some exceptions, such as transportation and staffing. In these cases, advances can reach or exceed 90%. Rates and advances vary based on volume, industry, and the other variables we discussed.

Additional resource: The Truth about Cheap Factoring Rates.

Looking for invoice factoring?

We are a leading provider of invoice factoring. If you would like a quote, fill out this form or call us toll-free at (877) 300 3258.

Marco Terry is the Managing Director of Commercial Capital LLC and has over two decades of experience in asset-based finance. He has worked with small and mid-sized companies across the United States, Canada, and Australia. Marco holds a Master of Science in Finance.