Many construction subcontractors have trouble paying employees or suppliers on time. Often, they have cash flow problems because clients pay invoices in 30 to 60 days while suppliers ask for quick payments. One way to fix this working capital problem is to use a revolving line of financing. This article explains how construction factoring can help quickly improve your company’s cash flow. It covers:

- Waiting 30 to 90 days for payment?

- The challenge of getting conventional financing

- What is construction factoring?

- How to qualify for construction factoring?

- Invoice verifications are key

- Is construction factoring right for your company?

1. Waiting 30 to 90 days for payment?

Construction subcontractors typically have to offer 30- to 90-day terms to commercial clients and general contractors (GCs). Commercial customers demand these payment terms as a condition of doing business with you. Unfortunately, there is little construction subcontractors can do about this. You must offer payment terms to clients if you want their business.

Construction subcontracting businesses are cash flow intensive. They have ongoing payroll and supplier expenses that have to be covered. Offering 30 to 90 days to pay an invoice can create cash flow problems for companies that aren’t well capitalized. Few companies in the construction industry have adequate emergency reserves. Consequently, offering terms puts them at risk of cash flow problems.

This problem can be solved easily with financing. However, this step presents a new problem. Getting financing is often a bigger challenge.

2. Getting financing is difficult for subcontractors

Getting a business line of credit is usually very difficult for companies in the construction industry. Lines of credit have stringent qualification requirements. Lenders typically require that the construction company:

- Have a long track record

- Be profitable

- Meet financial ratios

- Meet asset minimums

- Meet restrictive covenants

Most small and midsize subcontractors don’t meet the requirements to qualify for a line of credit. However, a commercial line of credit isn’t the only way to solve this problem. One alternative solution is to use construction factoring. It can provide a revolving line of financing that is tied to your accounts receivable.

3. What is construction factoring?

Construction factoring is a specialized factoring product that is customized for subcontractors. It improves your working capital by providing an advance against your invoices for completed work. An advantage of construction factoring lines is that they can handle progress payments, which conventional factoring lines can’t.

The facility improves your cash flow and puts your company on a stable financial platform, enabling it to complete jobs and take on new clients. Factoring allows you to keep offering payment terms while meeting your obligations.

Transactions are not structured as a loan. Instead, factoring companies buy your accounts receivable from creditworthy commercial clients and GCs. The facility is structured as a purchase rather than a loan. Consequently, it has simpler qualification criteria.

a) How does construction factoring work?

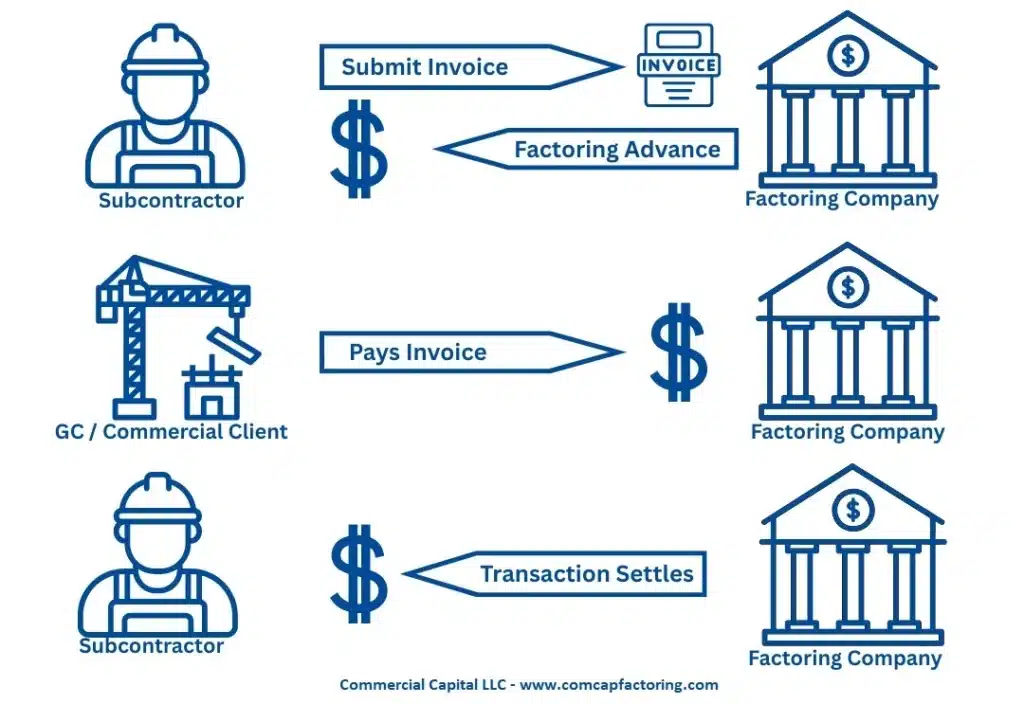

The factoring company buys your invoices in two installments. The first installment, called the advance, covers 70% to 80% of the value of the invoice, net of retainage. The advance percentage varies and is based on your company’s specific situation.

The finance company deposits the advance into your bank account shortly after they finance the invoice. The advance improves your cash flow quickly and is the main advantage of factoring. The remaining 20% to 30% is deposited in your bank account as a second installment once your GC or commercial client pays the invoice. The factoring fee is deducted from the second installment. The following image shows the key steps of the construction factoring process.

Read “What is construction factoring? How does it work?” to learn more.

4. Qualification criteria

The qualification criteria for construction factoring are similar to the requirements for regular factoring. However, there are new criteria that are specific to this product. Here are the five most important qualification requirements.

a) You must be a subcontractor

Construction factoring can be used only by subcontractors. It cannot be used by general contractors. This limitation is in place for two reasons. In most cases, a GC must get a bond for a specific project. The bonding company files a lien that encumbers the invoices associated with the particular project. This lien prevents the factoring company from buying those invoices.

The second reason is operational. The only way a factoring company could work with a GC is if the factoring company handles the payments and lien releases for all the GC’s subcontractors. Unfortunately, factoring companies don’t have the operational capabilities to perform these tasks.

b) You cannot subcontract work to others

Construction factoring can be used only by subcontractors that use their staff. It cannot be used by subcontractors that subcontract out parts of their work.

c) You must meet minimums

Most construction factoring companies have monthly minimums of $500,000, though some are higher. This requirement means that the subcontractors must invoice and factor above the minimum every month to stay compliant.

d) Your customers must have good business credit

Your commercial clients and general contractors must have good business credit. Factoring companies can only finance invoices payable by customers with good business credit. Business credit is determined using credit bureaus such as Dun and Bradstreet or Experian.

e) Your A/R must not be encumbered

Factoring companies can buy your invoices only if they are free of liens. Liens can come from bonding companies, finance companies (e.g., equipment financing), taxing authorities, etc. The factoring company will need a subordination if a lien encumbers your invoices.

f) Your invoices cannot have a “pay-when-paid” clause

Some general contracts have a “pay-when-paid” clause in their contracts. This clause means that the GC pays you only after they get paid by their customer. Unfortunately, factoring companies are unable to finance these invoices. The reason is that the end customer could withhold payment from a GC for issues unrelated to your company. Consequently, your payment is delayed even if your company delivers everything according to expectations.

The only way around this issue is to ask the general contractor to sign a waiver of that clause. In our experience, few GCs are willing to sign such waivers.

5. Invoice verifications

Factoring companies verify invoices before they fund them. This process is standard in the industry and ensures that:

- The invoice is due to be paid

- The work is completed

- There are no holdbacks

- There are no “pay-when-paid” clauses

In some cases, the factoring company may ask for a written confirmation of the verification. This request is common for invoices whose “pay-when-paid” clause has been waived.

6. Is construction factoring right for your company?

Construction factoring helps subcontractors who have cash flow problems because they cannot afford to wait to get paid by customers or GCs. It does not help if your company has financial problems for other reasons. In general, you should consider factoring if your company:

- Has creditworthy GCs or commercial clients

- Has cash flow problems because it offers payment terms

- Invoices a minimum of $100,000 per month

- Does not have serious issues

Can we help you?

We are a leading construction factoring company and can provide you with a competitive proposal. For more information, get an online quote or call us toll-free at (877) 300 3258 to speak with an expert.

Marco Terry is the Managing Director of Commercial Capital LLC and has over two decades of experience in asset-based finance. He has worked with small and mid-sized companies across the United States, Canada, and Australia. Marco holds a Master of Science in Finance.