An early payment discount is an incentive that companies receive from suppliers in exchange for a quick payment. It is usually offered by suppliers that need to improve their cash position. In this article, we discuss:

- Why are early payment discounts needed?

- How do they work?

- Who should get a discount?

- Advantages and disadvantages

- Are there better alternatives?

- Cost comparisons

- Advantages of using financing

- Making the decision

1. Why do you need early payment discounts?

Selling to commercial clients can be a challenge for small and growing companies. Most commercial and government clients have contract terms that allow them to pay invoices in 30 to 60 days. These terms can create cash flow problems for companies that can’t afford to wait for payment.

These cash flow problems can also affect growing companies that appear to be doing well financially. Sales may be growing, but collections lag behind expenses. As a result, expenses grow while your cash reserves shrink – at least initially. For a more detailed explanation about this scenario, read “Cash Flow Problems Due to Growth.”

There are several ways to correct this problem. The most common solution is to implement early payment discounts.

2. How do early payment discounts work?

Early payment discounts are simple to deploy and can produce quick results. Their main objective is to close the gap between invoicing and collections.

Clients are usually offered two options. They can pay the full amount on their usual terms or pay a discounted amount if they pay early. Offering a 2% discount for payment in 10 days is common. For example, if you provide a 2% discount and your usual terms are net 45 days, you would write “2%/10 – net 45” on the invoice. Other discount options include:

- 1%/10 – net 30

- 1%/10 – net 60

- 2%/10 – net 30

- 2%/10 – net 60

Each industry has its customary discounts and terms. However, they are negotiable. Consequently, negotiate the lowest possible discount for the quickest payment.

3. Who should get a discount?

Business owners sometimes offer these incentives to clients that pay very slowly, often when invoices are past due. This strategy exposes you to risk because these clients could also opt to take the discount and pay slowly. This situation happens often enough to warrant concern.

Instead, offer early payment discounts to clients that have a good track record of always paying on time. You can determine this by looking at your accounting system. However, consider reviewing their commercial credit first.

4. Advantages and disadvantages

While this solution can provide good results, it is not for everyone. Like every financial decision, its pros and cons must be considered. Discounts work very quickly, and you can often see results shortly after you begin using them. This is an important advantage for companies that have immediate cash flow problems. They are also easy to offer, and most clients like having the option to pay early in exchange for a discount.

However, this option has some critical disadvantages. These include:

a) They are optional

Taking the discount is optional. Your client chooses if to take the discount and when. Unfortunately, you never know for sure if a client will pay quickly until the payment arrives. This can make discounts somewhat unreliable.

Clients will also stop paying quickly during recessions and other difficult times. Consequently, you could end up in the same situation you were trying to avoid.

b) They are open to abuse

Some unscrupulous clients may abuse the discounts. They will take the discount but still pay on terms or late. This abuse puts your company in a difficult position because you have to attempt to collect that money.

c) They can be very expensive to offer

Offering terms can be expensive, especially if you have cheaper alternatives. Let’s take an example of a 2%/10 net-30 payment term. You are offering a 2% to accelerate your cash flow by 20 days. This translates to an approximate yearly financing cost of 36%.

Many small businesses think they don’t have other options, so offering a 2% discount is better than nothing. It’s certainly better than running into financial problems. Fortunately, other options can provide better results, as we will see in the next section.

5. Alternatives to early payment discounts

In principle, a bank line of credit is the best and cheapest option to handle the cash flow issues from slow payments. Unfortunately, qualifying for a line of credit is difficult. They are often out of the reach of smaller businesses. For smaller companies, the best alternatives are factoring, sales ledger financing, and asset-based loans

a) Factoring

Commonly referred to as “invoice factoring,” this solution allows companies to finance net-30 to net-60 invoices. Invoices are financed through a factoring company. The factor provides an advance using the invoice as collateral. Transactions are usually financed in two installments payments.

The first installment is called the advance and covers up to 90% of the invoice value. The advance is deposited in your bank account shortly after you finance the invoice. The remaining 10%, less the factoring fee, is deposited to your bank account when the client pays the invoice in full.

Qualifying for factoring is relatively easy. This makes it an excellent solution for small companies, startups, or companies that don’t qualify for bank financing. Factoring rates range from 1.18% to 3.5% per 30 days (prorated), depending on the transaction details. For more information, read “What is factoring?“

b) Sales ledger financing

Sales ledger financing is an alternative to factoring. It works similarly, though it more closely resembles a line of credit. It is usually offered to companies that have outgrown their factoring programs.

These programs are available to companies that invoice a minimum of $850,000 per month. They are usually priced using a prime rate + X% model. Sales ledger financing lines have more stringent requirements than factoring lines but not as stringent as other alternatives.

c) Asset-based lending

A third alternative is to use asset-based financing. Asset-based loans (ABLs) can be used to finance receivables, inventory, machinery, and other assets.

Many companies use ABLs specifically to finance their accounts receivables. Just like sales ledger financing, receivables-based facilities work much like a commercial line of credit. ABLs use a borrowing base certificate and don’t require as much direct management as factoring lines.

Most asset-based loans have a minimum size of $1,000,000 and can cover substantially higher amounts. Like sales ledger lines, they are priced using a prime + X% model. Generally, ABLs are cheaper than sales ledger financing lines.

For more information, read “What is an asset-based loan?“

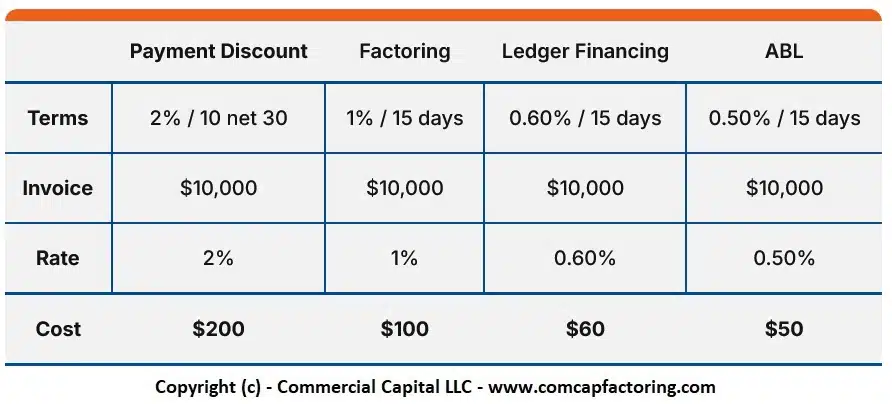

6. Cost comparison of all alternatives

Comparing the cost of early payment discounts against the various financing options can be challenging. Most solutions don’t have standard pricing, and the time frames of the cash flow vary. You will have to negotiate the best structure based on your specific situation.

The following chart shows a cost comparison using early payment discounts, factoring, sales ledger financing, and asset-based lending. Each line is priced at the approximate level for their entry point pricing.

| Payment Discount | Factoring | Ledger Financing | ABL | |

|---|---|---|---|---|

| Terms | 2% / 10 net 30 | 1% / 15 days | 0.60% / 15 days | 0.50% / 15 days |

| Invoice | $10,000 | $10,000 | $10,000 | $10,000 |

| Rate | 2% | 1% | 0.60% | 0.50% |

| Cost | $200 | $100 | $60 | $50 |

(Note: Table is scrollable left/right on mobile devices. Touch table if scrollbar does not appear. Click here for an image of the table.)

{kind=link}

The comparison is not a precise “apples-to-apples” comparison, but it shows a trend. In general, the relative price of financing is cheaper than the relative price of using early payment discounts. However, there is one important caveat.

The cost of early payment discounts is fixed and applies only if the client pays early. On the other hand, your cost of financing invoices increases the longer clients take to pay. Companies use financing to replace early payment discounts. Consequently, clients won’t have an incentive to pay early and will pay within their usual terms.

7. Are there advantages to using financing?

Using financing can be cheaper than providing discounts for early payments in some circumstances. However, this is not always the case. Consider these other advantages when making a decision.

a) Financing provides dependable cash flow

The most important advantage is that financing provides dependable cash flow. You no longer wait for a client’s payment or hope they took the early payment discount. This certainty enables you to grow your business more effectively.

b) Some lines have a selective option

Many factoring lines have a “selective” option that allows you to choose which clients and invoices to finance. Selective options provide you with a detailed level of control over your financing costs, enabling you to minimize costs.

c) Financing gets cheaper as your business grows

The pricing of financial lines is usually tied to your sales volume. The rate falls as your volume increases. Consequently, your per dollar cost decreases as your business grows.

8. What is your best option?

If your company has occasional cash flow problems that are not serious, offering early payment discounts should be your first choice. Discounts are not too expensive if used selectively and sporadically. Furthermore, they are very easy to implement.

If your company has recurring cash flow problems due to slow-paying clients, consider one of the previously discussed options. Smaller companies should first look into factoring. Larger companies, those that invoice at least $850,000, should consider sales ledger financing or asset-based financing.

Sales ledger financing lines are usually a better choice than asset-based financing, even though ABLs can be cheaper. Sales ledger lines are usually more flexible, have fewer covenants, and have fewer due diligence requirements. The benefits in ease and convenience are usually worth the slightly higher cost.

Lastly, if your company has serious financial problems, consider discussing your options with a CPA or finance specialist.

Need more information?

Do you have cash flow problems? We are a leading invoice factoring company and can provide you with competitive financing terms. For more information, get an online quote or call us toll-free at (877) 300 3258.

Marco Terry is the Managing Director of Commercial Capital LLC and has over two decades of experience in asset-based finance. He has worked with small and mid-sized companies across the United States, Canada, and Australia. Marco holds a Master of Science in Finance.