Getting financing has always been a challenge for construction subcontractors. Banks and financial institutions have strict underwriting criteria and work only with larger companies. This situation creates problems for subcontractors who need financing to run their companies.

This article discusses seven ways to finance a small subcontracting business. These options are available to small and midsize companies, and several options can be used at the same time.

1) Your clients

Clients can help you finance your company if they prepay part, or all, of their invoices. The prepayment provides your company with the funds to cover the expenses associated with the project. Getting your clients to prepay for some of the work is not easy. However, it can be done if your company provides a quality and valuable service.

Subcontractors with commercial clients usually give them 30 to 60 days to pay their invoices. Providing payment terms to commercial clients and general contractors is a standard industry practice. Unfortunately, it is also the source of many cash flow problems for construction subcontractors.

You can often get commercial clients to pay sooner if you offer an early payment discount. These programs offer clients a 1% to 2% discount on their invoices as an incentive if they pay within ten days. Your clients will appreciate this benefit since it increases their profits. If you time things correctly, some payments should come in before you have to pay expenses.

2) Leverage your suppliers

As we discussed in the previous section, proving payment terms is a common business practice. Your suppliers can also finance your company by providing you with 30- to 60-day payment terms. Basically, you ask suppliers to give you 30- to 60-day terms, just like you give to your commercial clients.

This strategy allows you to use the supplier’s product for up to two months before you pay for them. Coupled with prepayments, or early payment discounts, it can help ensure you get paid before you need to pay expenses.

Small subcontractors without a business credit history may have problems getting payment terms from suppliers. Fortunately, this problem can usually be fixed. Small subcontractors can often get credit from suppliers by building a track record of paying them on time. It will take some time and effort, but it’s worth it.

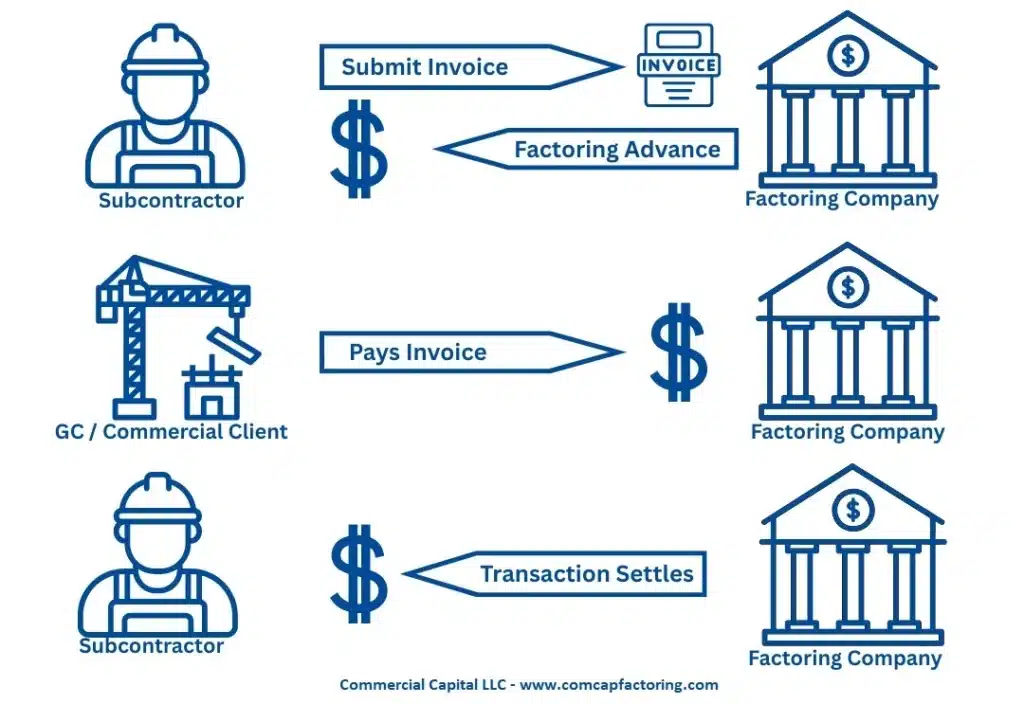

3) Finance your invoices

Companies whose cash flow problems are due to slow-paying invoices should consider construction factoring. Construction factoring is an increasingly popular financing option among subcontractors. It improves cash flow and provides a financial platform that can be used to grow the business.

Most factoring companies finance your invoices by purchasing them rather than offering a loan. This is because the transaction structure has simpler qualification requirements than conventional loans.

Transactions usually have two installments. Your company gets between 70% and 85% as a first installment shortly after financing the invoice. Once your end customer pays, you get the remaining funds, less the fee. The following diagram shows the key steps of the construction factoring process.

4) Finance your equipment

Construction companies that need to acquire equipment can use equipment financing. Equipment financing companies can provide funding to lease or buy the equipment you need for your company. Many of these programs have reasonable qualification requirements that are easier to get than conventional business loans. Loans and leases have advantages and disadvantages that depend on your circumstances. Consult a CPA to determine if a loan or lease works better for your company.

5) The Small Business Administration (SBA)

The SBA is a great source of financing that construction subcontractors often overlook. As a government agency that helps small businesses, the SBA has excellent programs designed to help small and midsize companies in most industries.

The SBA does not make business loans. Rather, the SBA guarantees loans for banks, which allows banks to lend to small businesses. These guarantees are an incentive for lenders and banks to provide financing to small companies.

The SBA’s Microloan program provides business loans and technical assistance to companies that need less than $50,000. Microloans have easy requirements and are often disbursed quickly. Furthermore, loan providers also offer business management and financial advice. These services are extremely useful for entrepreneurs. We highly recommend this program.

The SBA also offers other loan programs, namely the 7a Loan Program, which can help if you need a larger amount of money. However, getting this type of financing is more complicated and takes longer.

6) Your own resources

Subcontracting company owners can also use their personal resources to finance business operations. However, you must be careful to avoid draining your funds to the point you can’t pay your bills.

We suggest you speak with an expert (e.g., a CPA) before considering tapping into your home equity or retirement funds. You could jeopardize your home and/or your retirement. You want to avoid this situation for obvious reasons.

7) Friends and family

Many entrepreneurs also get financing by convincing friends and family to invest in their company. Friends and family can invest in one of two ways: they can buy equity in the business and get ownership or provide a loan.

Each option has its advantages and disadvantages. A loan is usually preferable because it allows you to keep control of the business. However, loans have to be paid back and are sometimes secured by personal assets.

Weigh the advantages and disadvantages carefully before taking money from friends and family. It can be a great source if used correctly and in the right circumstances. More often than not, entrepreneurs use this source incorrectly and run into problems. We usually advise against this option.

Speak to a CPA and an attorney before considering taking money from friends and family. You will need their help creating the right financial structure and drafting the required documents. Lastly, remember that accepting money from a friend or family member may put the relationship at risk. If the business fails, you could lose your business and your friend/family member.

Get more information

Are you looking for financing? We are a leading construction factoring company and can provide you with competitive terms. For more information, get an online quote or call us toll-free at (877) 300 3258.

Marco Terry is the Managing Director of Commercial Capital LLC and has over two decades of experience in asset-based finance. He has worked with small and mid-sized companies across the United States, Canada, and Australia. Marco holds a Master of Science in Finance.